AIM Dividend Monitor 2020

September 2020 / Link Group

AIM dividends set to fall by at least a third in 2020 following a record 2019 as COVID-19 crisis bites into company profits

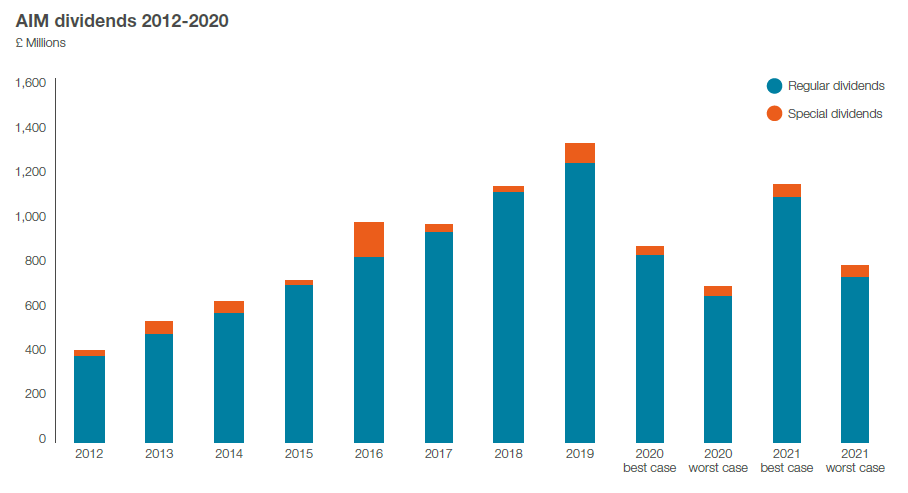

2019 saw record dividends on AIM

- Payouts jumped to a record £1.33bn in 2019, up 16.7% year-on-year on a headline basis

Q2 2020 and the impact of COVID-19

- Q2 payouts fell by a third, even after allowing for one-off dividends, takeovers and companies being promoted to the main market

- Two fifths of Q2 payers cancelled dividends outright and another tenth cut them, though some of the causes pre-dated COVID-19

- AIM dividends fell less than the main market, which saw underlying payouts halve – but this must be set in the context of the annual growth trend of 18% on AIM

Outlook

- Link Group’s best-case scenario sees AIM dividends falling 34% to £873m on a headline basis

- Link Group’s worst-case sees them dropping 48% to £698m

- The recovery to previous highs is likely to be 2022 or 2023 at the earliest

Having reached a new record in 2019, AIM dividends flatlined in Q1 2020 on the back of a weak UK economy before succumbing to the COVID-19 recession in the second quarter, according to the latest annual AIM Dividend Monitor from global financial administrators Link Group.

The second quarter usually marks a seasonal high point for dividends, so what happens in this period is very important for the whole year. It was also the quarter when companies began to react to the chilling effect of the government’s lockdown policy. Q2 AIM payouts fell by an unprecedented 33.6% on a headline basis to £266.8m. Special dividends supported the headline total. At £33m, they were almost five times larger than Q2 2019. Excluding specials, dividends fell 40.6% to £234.3m, a level last seen in mid-2016. The £107m decline was exaggerated by the promotion of Diversified Oil & Gas to the main market, and the takeover of SafeCharge and Manx Telecom, but on a like-for-like basis the decline was still over 33% year-on-year.

Two fifths of Q2 AIM payers cancelled their dividends outright, while another tenth reduced them year-on-year. Not all of these were due to COVID-19 however. For example, the biggest impact came from Eddie Stobart group, which was saved from administration late in 2019 by a capital injection from investors, but which naturally will not pay dividends during its turnaround period. The group was one of AIM’s top payers in 2018 and 2019 and accounted for one sixth of the total decline. Central Asia Metals also scrapped its payout for reasons of tough trading unrelated to the pandemic. Burford Capital, the second largest payer in Q2 2019, scrapped its dividend and reallocated the capital saved to its financing arm.

AIM dividends fell less in the second quarter than companies on the main market (where payouts halved) and a smaller proportion of companies made reductions. Two-fifths of companies reduced payouts on AIM compared to three quarters on the main market.

A culture of dividend paying has been growing on AIM. In 2019, 290 companies distributed cash to shareholders, up from 263 in 2018. The proportion paying has grown from 26% in 2012 to 35% last year. This compares to 80% on the main market. 2020 will see a break in this trend as the pandemic wreaks its historic disruption to all walks of life. It will take time for a full recovery to take place, but we would expect 2020 to mark only a temporary low point.

According to our

most recent UK Dividend Monitor,

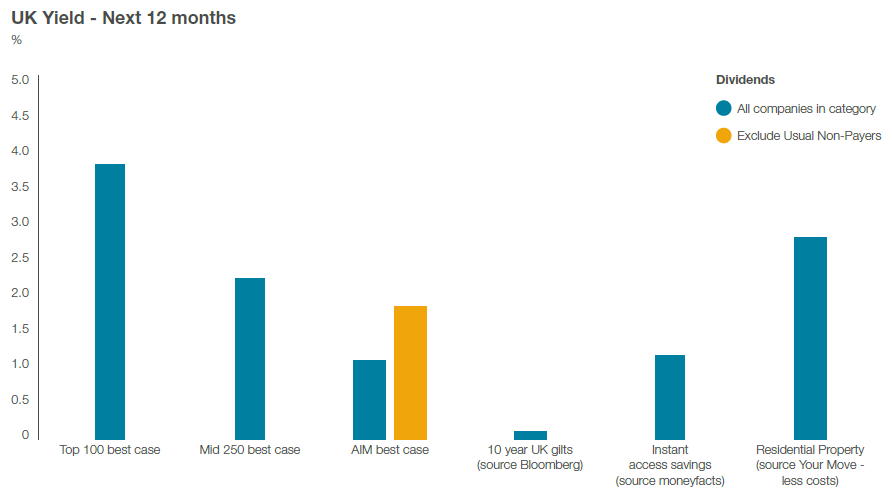

the main market will yield 3.6% over the next twelve months if Link Group’s best case materialises, or 3.3% if Link Group’s worst case does.

AIM is a lower-yielding market, even in normal times. Over the next twelve months, Link Group expects AIM shares to yield 1.1% on a best-case basis or 0.7% on a worst-case basis. This figure is artificially distorted by the two thirds of AIM companies that do not normally pay dividends. If these are excluded (but not those that only dropped out in 2020), then the best-case yield is 1.9% and the worst case 1.1%.

Link Group expects total AIM payouts to drop by 34% on a best-case basis to a headline £873m in 2020, slightly better than Link Group’s best-case scenario for the main market (-38%). This would reduce AIM’s dividends to a level last seen around the middle of 2016. The worst-case scenario sees them falling by 48% to £698m (worse than the main market at -42%), a level last seen in late 2014. The greater uncertainty over the response from AIM companies explains the wider range between the best and worst case than for the main market.

Susan Ring, CEO of Corporate Markets, Link Group said: “Even before the pandemic struck, late 2019 and 2020 were set to be different. The UK economy had already weakened significantly by the end of 2019. AIM companies tend to be more sensitive to the economic cycle because the sector complexion means defensive firms are relatively under-represented. Industrials, financials, and resources companies feature prominently on AIM. These groups find their profits rising and falling with the fortunes of the wider economy more than, say, tobacco or food producers, whose earnings are relatively insulated. On the main market, roughly half the total payout comes from defensive sectors, but on AIM just one quarter does. The rest are more exposed.

“The fact that AIM dividends fell less than the main market must be seen in the context of long-term AIM underlying dividend growth of 18% per annum. The change from an increase of that size to a sudden decline of one third is consistent with the magnitude of main market dividend cuts we have reported in our main UK Dividend Monitor. What’s more, only a minority of AIM companies pay dividends at all, and those that do will tend to be the ones with deeper pockets. Lower payout ratios in the first place play a role too, as growth companies tend to pay lower dividends in the early days. We think it likely that AIM companies may also have simply been slower off the mark than larger UK plcs which reacted with lightning speed in cancelling payouts. This may well mean a delayed impact over the coming quarters, not least as the impact on profits becomes a reality rather than a prospect.

“2020 will take the biggest hit. Our estimates come with a health warning, given the relative lack of visibility in AIM dividends and the unusually large uncertainty in the wider environment. AIM’s payouts will certainly bounce back in 2021, but even if they return to trend growth thereafter, they are unlikely to top 2019 until 2022 or 2023 at the earliest. This AIM recovery will be faster than on the main market, where it will take time to make up for the loss of £7.8bn from Shell alone.”

Download the full AIM Dividend Monitor hereOpens in new window