UK Dividend Monitor Q1 2020

April 2020 / Link Group

.jpg)

UK companies scrap one third of 2020's remaining dividends as COVID-19 crisis batters business

Every quarter for the last ten years, the Dividend Monitor has tracked the income paid to shareholders by the UK’s listed companies. It has picked through every payment made during the period, identified the key trends, and maintained a forecast for each year with a reliable reputation for accuracy. Even during the global financial crisis and subsequent recession we were able to report on UK plc’s dividends in the normal way.

The current crisis is not normal, even by the standards of crises. We are therefore temporarily adapting the Dividend Monitor to tackle how the pandemic is affecting UK payouts, with a much shorter focus on the quarter that has just been. The crisis will pass, and the Dividend Monitor will return to normality, but for now we hope you find our new insight helpful.

- 45% of UK companies have already scrapped payouts to shareholders

- £25.4bn of cuts sure to hit this year, equivalent to one third of the April to December total

- A further £23.9bn are at risk, but an encouraging £31.1bn are likely to be safe

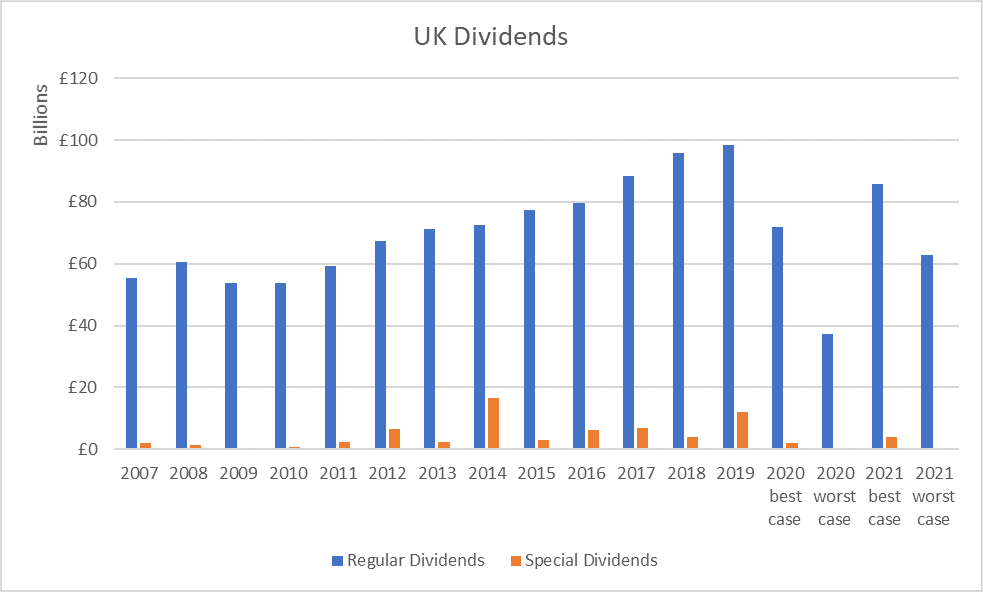

- Four scenarios for 2020 (with Q1 dividends safely in the bag)

- Best case - dividends fall 27% to £71.9bn

- Worst case - dividends fall 51% to £48.0bn

- Realistic, upper bound - dividends fall 32% to £67.3bn

- Realistic, lower bound - dividends fall 39% to £60.0bn

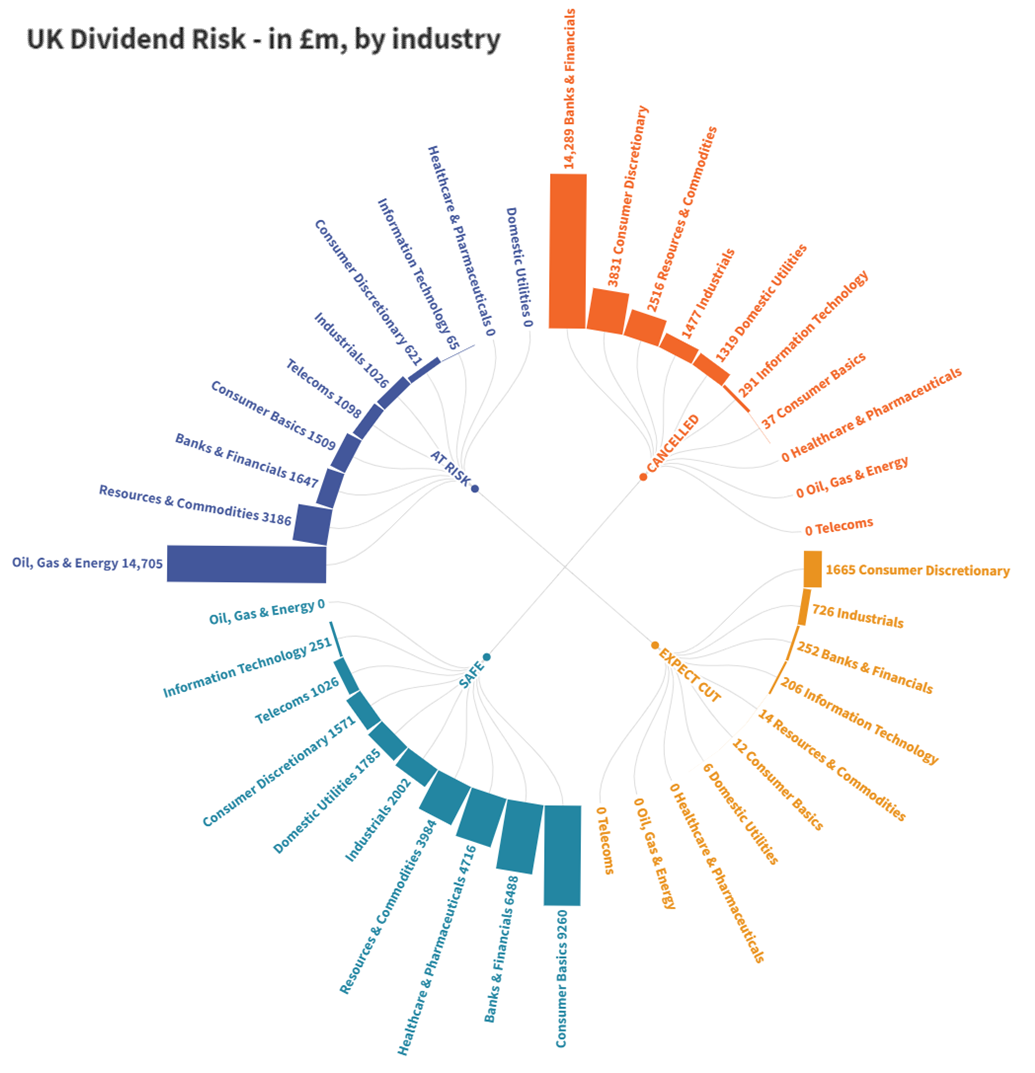

- Covid-19 Impact by Sector

- Biggest impacts comes from banks, slashing by £13.6bn

- The big mining sector is seeing a mixed impact

- Liklihood of cuts from the oil giants is hotly disputed in the market

- Classic defensive dividends are more likely to be safe - e.g. food retail, food, drink & tobacco, basic consumer goods and healthcare

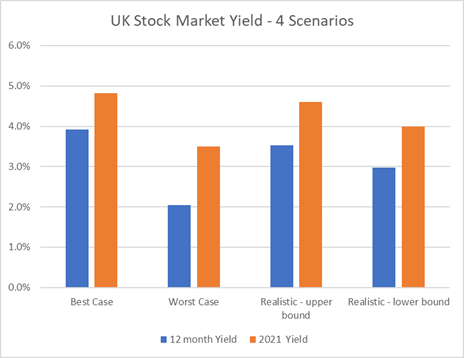

- Yield - a way to understand share prices

- Our four scenarios show that the 2020 yield is very uncertain

- But 2021 gives a much clearer picture, implying UK shares are at worst, fairly valued at present and could have significant upside

The latest UK Dividend Monitor from Link Group has comprehensively analysed the impact of the Covid-19 pandemic on UK dividends. Within a few days from the middle of March, UK companies scrapped payouts to shareholders worth a staggering £25.4bn between now and the end of December this year. This represents one third of the dividends Link had expected (before the crisis struck) UK plc to pay over the rest of this year. By April 5th, 45% of Britain’s listed companies had already axed their payouts or are certain to do so, an unprecedented figure.

Link flags a further £23.9bn it judges to be at risk for this year, equivalent to 29% of 2020’s April-December payouts. The rest, just £31.1bn, Link judges to be safe.

Link is withdrawing its formal forecast for 2020 until the depth and duration of the lockdown and associated economic impact becomes clearer. In its place, Link introduces four scenarios to help investors understand how 2020 could shape up. These scenarios acknowledge that £17.5bn of dividends were already in bag, having been paid in Q1.

In value terms, the biggest confirmed impact comes from the banks, slashing £13.6bn off this year’s total. The next largest comes from the mining sector, mainly thanks to Glencore. More mining dividends are at risk, but some we judge to be safe. The safest groups include food, drink & tobacco, utilities, food retailers, healthcare and basic consumer goods. These are all the classic defensive sectors, and we have already seen how they have continued to see great demand for their goods and services as the pandemic has unfolded. In the At Risk group, half the value is made up by the oil sector. Oil prices are low, hit by a Saudi v Russia price war. Market opinion is split down the middle on the likelihood the oil majors will cut their payouts – even if they do, full cancellation is highly unlikely. (You can find full sector breakdowns and more charts in our full report.)

Over the next twelve months, Link’s best-case scenario implies UK shares will yield 3.9% (£3.90 for every £100 of shares owned), attractively above the 3.5% average for the last thirty years. Link’s worst-case scenario puts the same figure at a disappointing 2.0%, in line with the lowest level reached in 2000, when the dotcom boom was riding high. The upper bound realistic scenario suggests 3.5%, in line with the long-run average. These scenarios suggest the UK market is either: a little undervalued and so could rise, is fairly valued, or is rather overvalued and so could fall. Not very helpful.

It is therefore important to look beyond the next twelve months, given that this is such an unusual year. Link has made some broad-brush assumptions about what 2021 might look like. If we imagine the banks return payouts to near full strength next year, and half of all the other cancelled dividends are restored, then a more realistic best-case yield is 4.8%, suggesting the market is severely undervalued at the moment and so presents a good buying opportunity. Link’s worst-case for 2021 suggests the market is now fairly valued.

Kit Atkinson, Head of Capital Markets for Corporate Markets EMEA at Link Group, said:

"Even as we face the deepest recession since the second world war, investors can take comfort from the knowledge that tens of billions of pounds of dividends will still be paid this year. More importantly, they will bounce back next year, even under quite bearish scenarios. Dividends really matter – not only do they provide income for pensioners and many other types of investor, but they also underpin share price valuations.

Some of the cancellations for this year are very necessary to protect companies – investors have responded well on the whole. For many, public relations are playing a role. Any company taking public money in one of the support schemes, either via government-backed loans or via taxpayer-funded salaries for furloughed workers would naturally face a public outcry if it continued payouts to shareholders. The banks are in a separate group. They are very well cushioned by strong balance sheets and could afford to pay dividends. But political influence has been brought to bear, and the banks have demurred for now.

We have no crystal ball but newsflow is sure to get worse before it gets better. The exceptional uncertainty explains why stock markets have fallen so far, so fast. Stock markets always try to get ahead of events and they are already pricing in a lot of bad news. If the damage to the economy truly can be limited by government action and if the economy can escape the prospect of a protracted depression, it’s clear markets can recover sooner and further. If the news turns out to be worse, they could decline further.”

A word about Q1’s results

First-quarter dividends were almost entirely unscathed by the crisis. They were, however, relatively weak reflecting the earnings recession already underway in the UK, even before the pandemic struck. They fell 11.0% on a headline basis to £17.5bn, but the severity of the decline was exacerbated by much lower one-off special dividends. Underlying payouts dropped 0.7% to £17.3bn. This was the second consecutive quarterly decline in underlying dividends. The last time this happened was during the global financial crisis.

Download the full reportOpens in new window