UK Dividend Monitor Q3 2020

October 2020 / Link Group

.jpg)

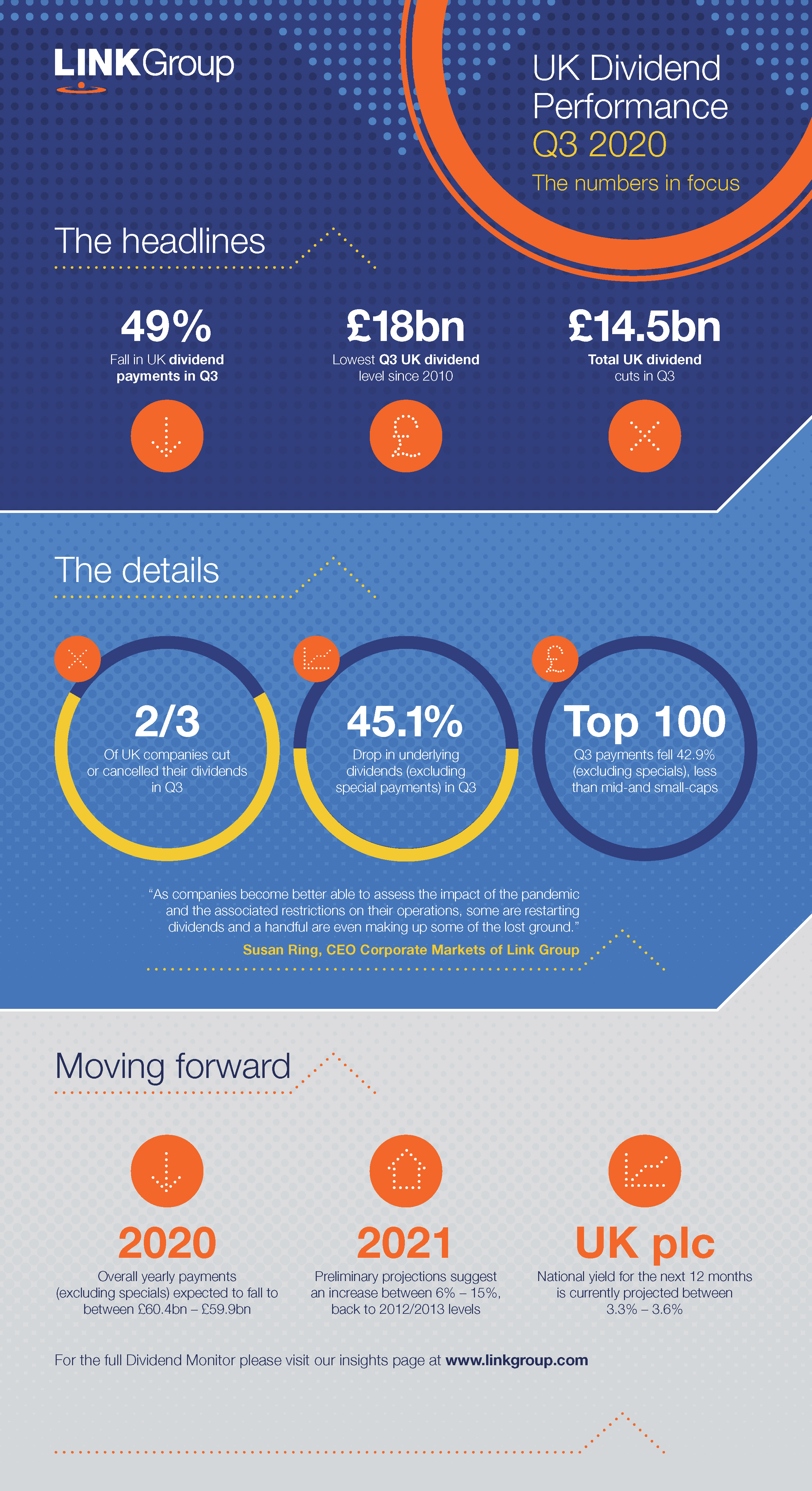

UK dividends halve in Q3, but the green shoots of recovery are beginning to show

- UK dividends fell 49.1% in Q3, dropping to £18.0bn, the lowest Q3 total since 2010, but the

decline was less severe than Q2

- Underlying dividends (which exclude special payments) fell 45.1% to £17.7bn

- Two thirds of companies cut or cancelled their payouts, less than the three quarters that did so in Q2

- Cuts totalled £14.5bn in Q3 - banks accounted for almost two fifths, oil companies another fifth,

and mining one eighth, but travel and leisure and retailers were worst hit

- Positive signs are emerging – some companies are restarting payouts

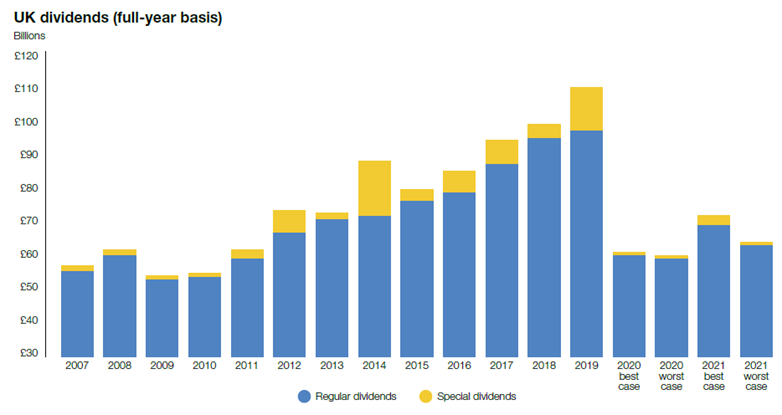

- For 2020, Link Group expects UK dividends (excluding specials) to fall to £60.4bn on a best-case

basis and £59.9bn on a worst-case basis, a decline of 38.7% and 39.2% respectively – exactly

halfway between April’s initial best- and worst-case scenarios (-27% to -51%)

- For 2021, Link Group pencils in a preliminary best-case increase of 15% and a worst case of 6%, taking

payouts back to levels last seen in 2012 and 2013

The UK’s dividend picture brightened a little in the third quarter, according to the latest UK Dividend

Monitor from global financial administrators Link Group, though only in the context of the record falls in

payouts that the 2020 crisis is delivering for shareholders. Q3 dividends slumped by 49.1% on a headline

basis to £18.0bn, the lowest Q3 total since 2010 when the UK was suffering the aftermath of the Global

Financial Crisis (GFC). Though by any normal standards a fall of this magnitude is terrible for investors,

it is significantly better than the 57.2% drop in the second quarter.

On an underlying basis, which excludes special dividends, payouts fell by 45.1% to £17.7bn, compared to

a 50.2% decline in the second quarter.

Overall, just under half of companies cancelled their dividends altogether in Q3, while a further fifth cut

them. This means that almost two thirds of companies cut or cancelled their payouts, in line with Link

Group’s expectations. In the second quarter, a staggering three quarters of companies cut or cancelled

payouts.

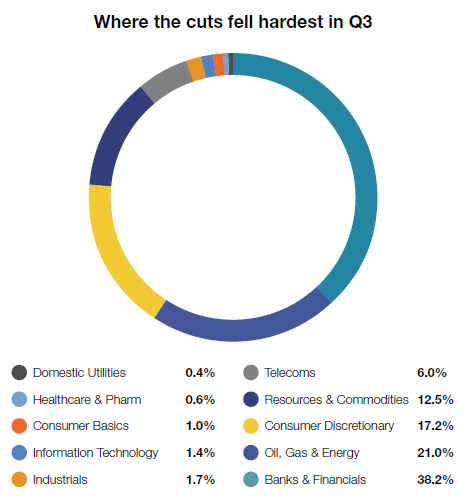

Of the £14.5bn of cuts in the third quarter, banks accounted for almost two fifths, as they remain

barred from paying dividends by the Bank of England. The oil sector contributed another fifth and mining one

eighth, though gold miners bucked the trend by paying sharp increases.

The airline, travel and leisure sector, general retail, media, and housebuilding and consumer goods and

services bore the brunt of the lockdown measures. Travel and retail payouts fell 96% year-on-year in Q3,

while those from the media and housebuilding and consumer goods and services sectors were down by two

thirds.

Only two sectors, the classically defensive food retailers and the basic consumer goods, delivered

year-on-year increases, though only just. A really positive sign came from BAE Systems and engineering

concern, IMI, becoming the first companies to catch up on all the dividends missed year-to-date. Berkeley

Group, which had rescinded a big special payout earlier in the year paid a very large interim, five times

bigger than 2019, to make up some of the lost ground. Others, like Direct Line, restarted their payouts.

In addition to the reductions in underlying dividends, one-off specials were also sharply lower, falling by

£2.8bn or 90% to £299m. Even so, this was a little better than we expected.

As in the second quarter, top 100 payouts fell by less than their small- and mid-cap counterparts in the

third. Excluding special dividends, payouts from the top 100 fell by 42.9%, from mid-caps by 60.4% and from

smaller companies by 69.5%.

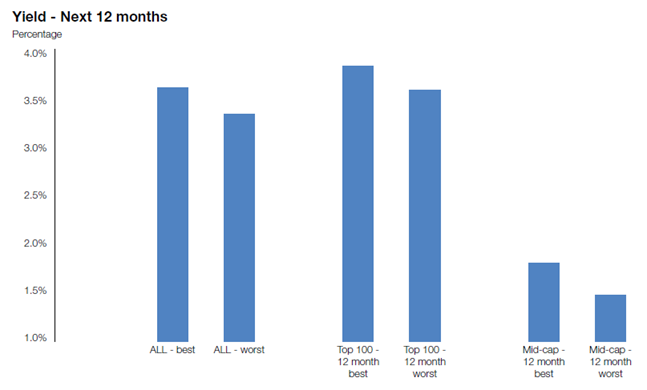

UK shares will yield 3.6% in a best-case scenario and 3.3% in a worst over the next twelve months.

Link Group now has excellent visibility on the prospects for the rest of 2020 and has therefore almost

eliminated the gap between its best- and worst-case scenario. Link now expects UK dividends (excluding

specials) to fall to £60.4bn on a best-case basis and £59.9bn on a worst-case, a decline of

38.7% and 39.2% respectively. This puts the likely outturn for 2020 exactly mid-way in Link Group’s

original April range, estimated at the moment of greatest uncertainty for UK companies. On a headline basis,

which includes special dividends, the 2020 decline is set to be between 44.6% and 45.2%, yielding

£61.2bn or £60.6bn respectively.

For 2021, Link Group pencils in a preliminary best-case increase of 15% and a worst case of 6%, taking

payouts back to levels last seen in 2012 and 2013.

Susan Ring, CEO Corporate Markets of Link Group said: “UK plc is not out of the woods,

but the trees are perhaps thinning a bit. Our worst-case scenario has steadily improved all year and though

UK investors face a historic decline in their income this year, the worst is now behind us. As companies

become better able to assess the impact of the pandemic and the associated restrictions on their operations,

some are restarting dividends and a handful are even making up some of the lost ground.

“Looking ahead there is still huge uncertainty. With the pandemic showing no sign of abating and no

hoped-for vaccines likely to be distributed for at least several months yet, governments are trying to walk

the tightrope of using prolonged restrictions to limit healthcare caseloads without destroying even more of

the economy and creating even more unintended consequences for health in other ways.

“The fourth quarter this year and the first quarter next are set for further sharp declines, but from

April onwards, the anniversary of the lockdown, the comparisons will start to look more favourable and we

expect to see a bounce-back begin. Oil dividends will not increase significantly (if at all), however, so

the big question will be whether the Bank of England permits the banks to begin distributing again. Beyond

the obvious economic impacts on their trading, the extent to which companies in other sectors have taken

government support will influence their freedom to pay shareholders too.

“There’s no doubt we have a long road ahead before dividends return to pre-pandemic levels, but

there is now at least a signpost to the route that will take us there.”

Download the full report hereOpens in new window