UK Dividend Monitor Q4 2019

27 January 2020 / Link Group

UK dividends soared to new record in 2019, but 2020 is set for declines

-

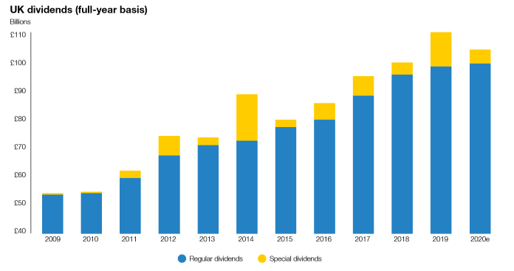

UK dividends jumped 10.7% to a record £110.5bn in 2019, boosted by an exceptionally large £12.0bn of special dividends

-

Underlying dividends (which exclude specials) rose just 2.8% to £98.5bn, the slowest increase since 2014

-

On a constant-currency basis, underlying growth was just 0.8%, once FX gains were excluded, the slowest since 2016

-

The big engines of dividend growth over the last three years – miners and banks – are less likely to propel dividends in 2020

-

The stronger pound and likely lower special dividends will also depress growth

-

Link forecasts headline dividends to fall 7.1% to £102.7bn in 2020 and underlying payouts (ie excluding specials) to fall 0.7% to £97.9bn, equivalent to an increase of 1.1% on a constant-currency basisUK shares are set to yield 4.1% in 2020. The top 100 will yield 4.2% and the mid-caps 3.0%

UK dividends jumped to a new record in 2019, according to the latest Dividend Monitor from Link Group. They rose 10.7% in headline terms to £110.5bn, in line with Link’s forecast for the year. This is more than double the level they reached a decade ago. To put this huge sum into context, for every £20 invested in the UK stock market at the beginning of 2019, investors earned an average of £1.02 in income from their shares.

The dramatic headline increase belied a more muted underlying picture, however. Once exceptionally large special dividends totalling £12.0bn were excluded, underlying growth was just 2.8%, the slowest increase since 2014. The underlying total was £98.5bn.

Two fifths of UK dividends are declared in US dollars, so the changing exchange rate makes a significant impact on the sterling value paid. The pound was significantly weaker in 2019 compared to 2018, and this inflated the value of dividends in sterling terms by £2.4bn in the first three quarters of the year. This was enough to boost the headline total by over two percentage points and accounted for almost three quarters of the underlying (i.e. excluding special) dividend growth in 2019. In fact, if exchange-rate effects are excluded, underlying growth was just 0.8% on a constant-currency basis, and dividends actually fell in the second half of the year.

Special dividends are by their very nature unpredictable. They tripled year-on-year to £12.0bn, the second-highest level on record as companies across a wide range of sectors sought to return excess cash to shareholders. Mining, banks and IT accounted for three quarters of the total paid, but housebuilders, hotel and leisure companies, and industrials also made a significant contribution.

Over the course of the full year, the top 100 companies performed more strongly on an underlying basis than their mid-cap counterparts, many of which suffered from the relative weakness of the UK economy. But the top 100 growth rate was flattered by exchange-rate effects (the FX effect on mid-caps is negligible). Neither group did well once special dividends and exchange rates were factored in.

The biggest paying sector, oil, gas & energy showed no growth in 2019 as companies use higher oil prices to rebuild dividend cover. Mining dividends, boosted by huge specials from Rio Tinto and BHP, made the largest contribution to growth, up by two fifths. The miners have provided the main engine of UK dividend growth in the last four years, increasing their payouts six-fold since the commodity slump of 2015-2016. The banking sector also made a significant contribution to growth in 2019. Banking dividends rose by a third to £15.6bn, making 2019 the first year to see larger payouts than 2007, indicating just how long it has taken for the sector to recover from the financial crisis.

The weakest performance came from the telecoms sector which is suffering from heavy investment needs and weak pricing. The total paid fell by over a quarter year-on-year, following a steep cut from Vodafone, though most companies in the sector either reduced their dividends or only managed to hold them steady.

For the year ahead, UK dividends face significant headwinds. Link does not expect such large special payouts, and if the pound maintains the higher levels at which it ended the year, it will reduce the translated value of payouts in 2020. Link’s preliminary 2020 forecast is for headline dividends to fall 7.1% to 102.7bn. Excluding special dividends Link expects underlying payouts to fall 0.7% to £97.9bn, equivalent to a 1.1% increase on a constant-currency basis, similar to the muted growth rate achieved in 2019.

Based on Link’s forecast for 2020, UK shares are set to yield 4.1% in 2020. The top 100 will yield 4.2% and the mid-caps 3.0%.

Michael Kempe, COO of Link Market Services, said:

'The spice of huge special dividends and the zest of big exchange-rate gains enlivened what was in truth a rather bland year for UK dividends. 2020 is not set for the same superficial excitement.

'The UK and global economies are set for a slightly better 2020 than 2019, and the squeeze on profits for UK mid-caps is likely to moderate, which should herald a modest turnaround in dividends from this group of companies.

'The outlook for the top 100 is much more important, however. Oil prices have jumped recently on rising tensions in the Middle East but this is unlikely to lead to increases in dividends from the sector.

'With payouts from the UK’s other biggest payers also unlikely to move very much and the big mining groups no longer providing the engine of dividend growth that drove UK dividends over the last three years, we do not expect significant increases from the top 100 either.

'More importantly, UK dividends face the significant headwinds of a stronger pound, and the likely decline of special payouts to more normal levels.'

Download the full reportOpens in new window