UK Dividend Monitor Q4 2020

January 2021 / Link Group

COVID-19 slashed UK dividends by two fifths in 2020 to levels last seen in 2011, as outlook for 2021 darkens

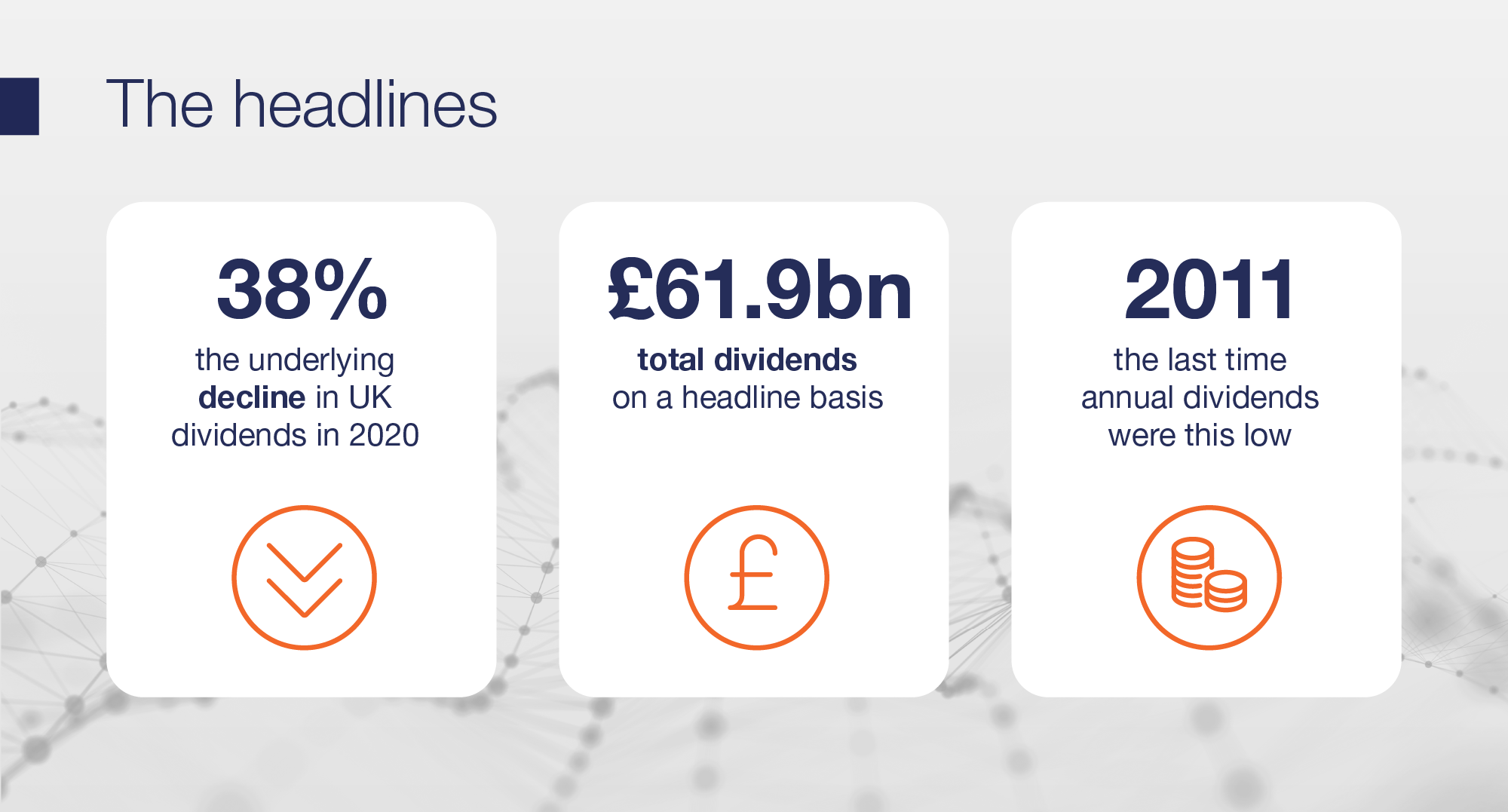

- 2020 dividends fell 44% to £61.9bn on a headline basis, the lowest annual total since 2011

- Underlying dividends (which exclude special payments) fell 38.1% to £61.1bn

- A better than expected Q4 was boosted by suspended payouts being restored, helping 2020 beat our revised best-case forecast by a whisker

- Two thirds of companies cancelled or cut their dividends between Q2 and Q4

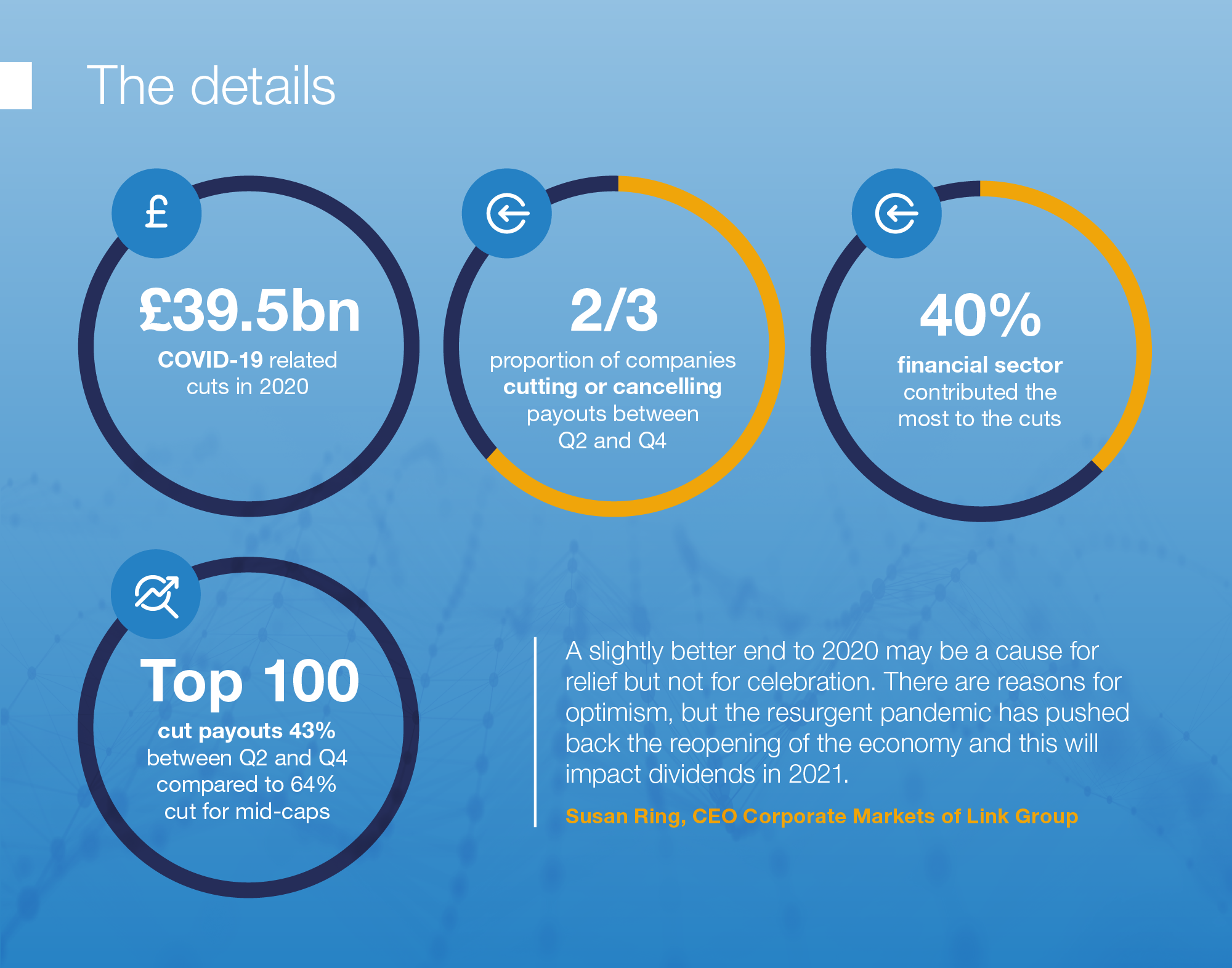

- COVID-19 cuts totalled £39.5bn (excluding specials) in 2020

- Financial sector contributed two fifths of the cuts, mainly owing to PRA prohibition on banking dividends

- Oil dividend cuts accounted for another fifth

- Top 100 payouts fell less than mid and small-caps, down 35% for the whole year, while mid-caps saw them drop 56%

- For 2021, Link Group expects a best-case increase of 8.1% on an underlying basis, yielding a total £66.0bn; headline dividends (which include specials) would rise 10.0%

- In a worst-case scenario payouts could fall again in 2021, dropping 0.6% to £60.7bn on an underlying basis, or £61.5bn including special dividends

- Link Group does not expect UK dividends to regain previous highs until 2025 at the very earliest

Eight years of growth was wiped off UK dividends in 2020, according to the latest UK Dividend Monitor from Link Group. Headline dividends fell 44% to £61.9bn, or 38.1% to £61.1bn on an underlying basis which excludes one-off specials. The total just beat Link Group’s revised best-case forecast for the year, thanks to a stronger than expected fourth quarter, which saw a number of companies such as Sainsbury’s and Ferguson restore payouts they had suspended earlier in the year.

COVID-19 cuts started at the beginning of Q2 and reached £39.5bn by the end of the year. Between Q2 and Q4 an astonishing two thirds of companies cancelled or cut their payouts (47% and 20% respectively), just over a quarter increased them, and the remainder held them steady.

By far the biggest impact came from the financial sector, accounting for two fifths of the COVID-19 cuts between April and December. £16.6bn of dividends were cut or cancelled. The outright cancellation of banking dividends accounted for four fifths of this, owing to the outright cancellation of banking dividends. Across the rest of the financial sector payouts fell by a third, slightly better than the wider market.

The next biggest impact was from the oil sector, costing shareholders £8.0bn in lost income. Having struggled to sustain their very large payouts in recent years, the UK’s oil majors took this opportunity to reset their dividends to more sustainable levels, collectively three fifths lower than before. They can now grow from this lower level, but since this sector has historically paid the highest dividends, this big reduction largely explains why it will take many years for UK plc dividends to regain previous highs. Shell has already made a small symbolic increase and we do expect further progress over time.

Almost a tenth of the cuts were made by mining companies, whose dividends fell by two fifths. Glencore’s £2.2bn cancellation made the biggest impact. Miners often pay special dividends but these were sharply curtailed too.

Apart from the banks, companies dependent on discretionary consumer spending made the biggest percentage cuts. Altogether, the various consumer discretionary sector payouts fell by £5.5bn, a three quarters decline. In this group, retailers and the airline, leisure and travel sector saw falls of more than 95%.

The classically defensive sectors of healthcare, basic consumer goods, food producers and food retail were true to type in 2020. Their dividends were flat or only slightly down between Q2 and Q4.

Despite the steep cuts by the banks, oils and miners, dividends from the top 100 have been less severely impacted by the pandemic than the mid-250. 53% of the top 100 cut or cancelled payouts between Q2 and Q4 compared to 63% of the mid-250. For the full year, the top 100 saw underlying dividends fall 35% while the mid-caps saw them drop 56%.

Both higher share prices and a lower forecast for dividends mean a compression of the prospective yield on equities. Based on Link’s best-case scenario for 2021, UK equities will yield 3.1% or 2.8% if our worst case materialises.

For 2021, the resurgent pandemic and renewed lockdown has delayed the recovery in dividends. Link expects 2021 payouts to rise 8.1% on an underlying basis, yielding a total of £66bn on a best-case scenario. Special dividends could take this to a headline £68.1bn, an increase of 10%. But in a worst-case scenario, payouts could fall again in 2021, dropping 0.6% to £60.7bn on an underlying basis, or £61.5bn including special dividends.

Susan Ring, CEO Corporate Markets of Link Group said: “A slightly better end to 2020 may be a cause for relief but not for celebration. This was a dreadful result for UK investors, especially those for whom dividends are a major source of income. UK payouts have been more severely impacted than in most comparable countries because of their heavy concentration in the hands of just a few very large companies, mainly in the oil, mining and banking industries – all sectors that have had to cut dividends steeply.

There are reasons for optimism, but the resurgent pandemic has pushed back the reopening of the economy even further, especially in the UK. We still believe the worst is past, but a new lockdown means our expectations for 2021 are significantly more subdued. The biggest upside will come from the banks. They will only partially restore their dividends, but it matters more how quickly they do so, rather than exactly how much they pay. By contrast, the £11bn reduction in oil dividends by March will take several years for the wider market to make up.

The social and economic scars of COVID-19 will be deep. We think it is highly unlikely dividends can regain their previous highs until 2025 at the earliest, and potentially even a year or two after that. We’ll keep you posted.

Download the full report hereOpens in new window